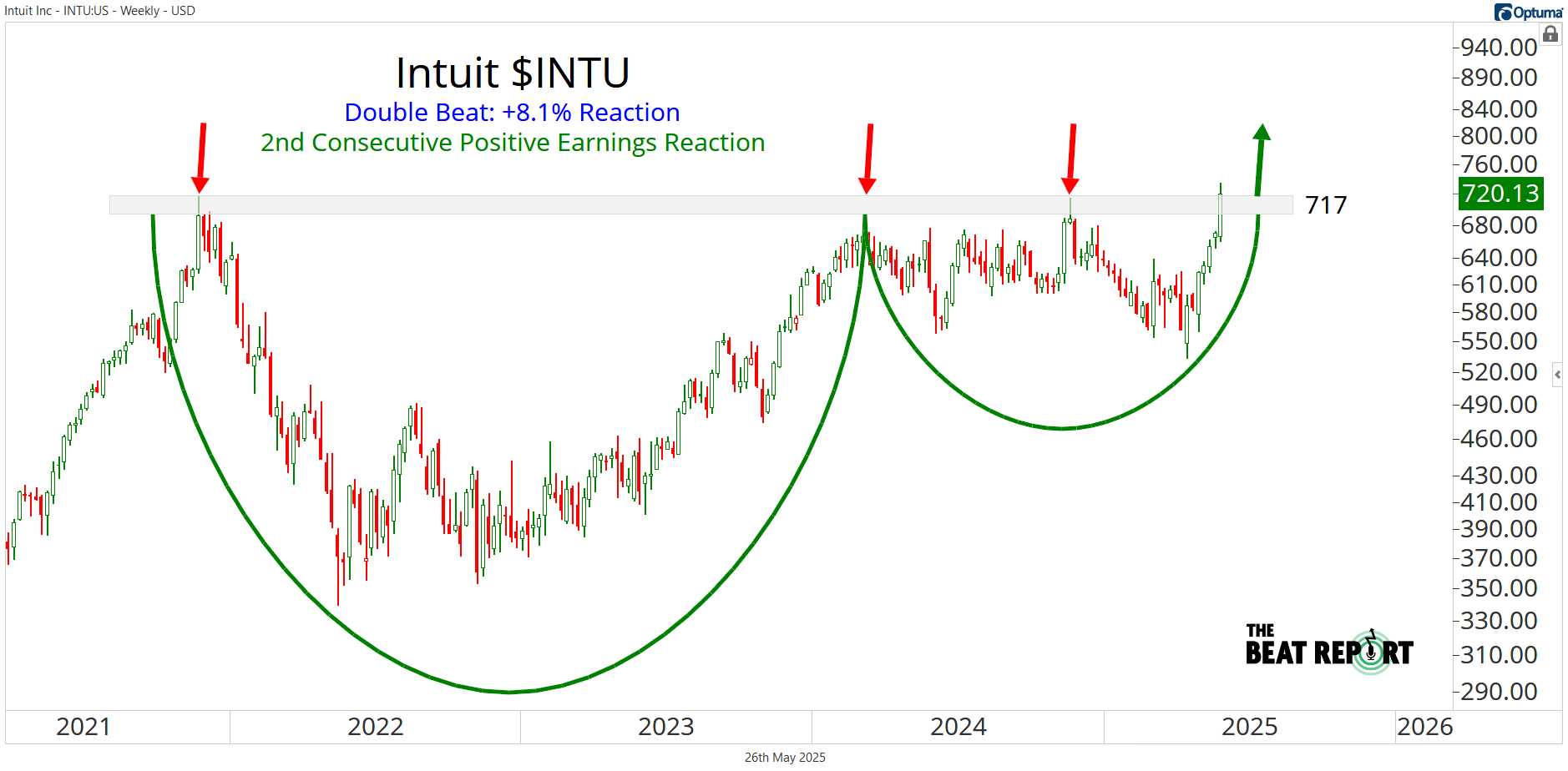

Intuit $INTU posted a double beat this quarter, exceeding revenue and earnings expectations.

Their strength comes from multiple engines:

Small Business and Self-Employed Group revenue jumped, fueled by growth in QuickBooks Online and payroll services.

TurboTax remained a cash machine during tax season, reinforcing Intuit’s dominance in consumer finance.

And Mailchimp and Credit Karma continued to expand their roles as critical tools for small business marketing and personal finance.

Management also raised full-year guidance across the board, a signal of confidence to the market.

In an environment where many software names are struggling to justify premium multiples, this company stands out for its consistency, diversification, and cash flow strength.

This report was just the latest reminder of why Intuit is one of the most valuable software companies in the world.

So what else did we learn from Friday's earnings reactions? Let’s dive into the details.

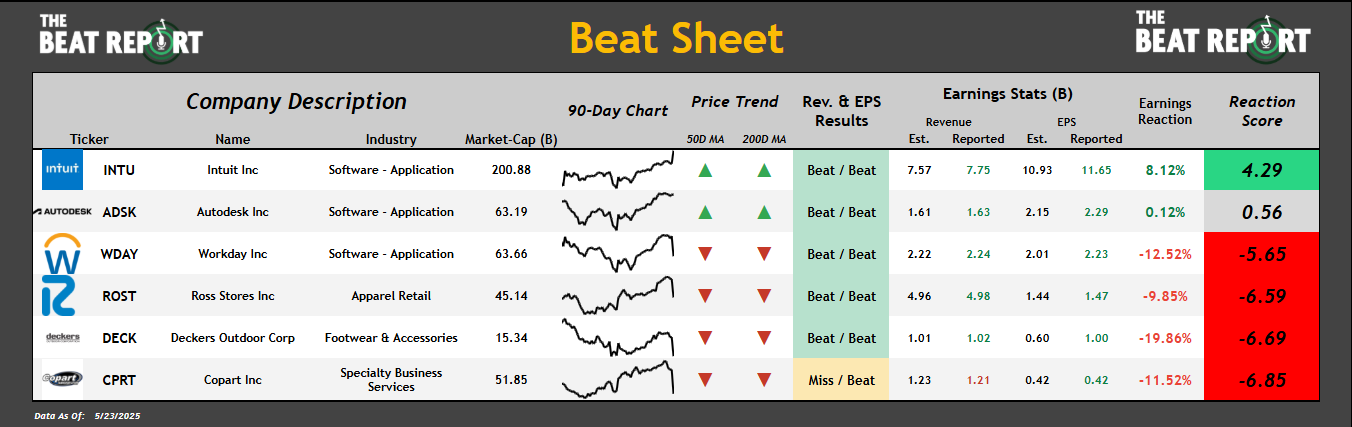

Here are the latest earnings reports from the S&P 500 👇

*Click the image to enlarge it

Intuit $INTU had the best reaction score after reporting a double beat.

The company reported revenues of $7.75B, versus the expected $7.57B, and earnings per share of $11.65, versus the expected $10.93.

Copart $CPRT had the worst reaction score after reporting mixed results.

The company reported revenues of $1.21B, versus the $1.23B estimate, and earnings per share of $0.42, which met the market's expectations.

Now let's dive into the data and talk about what happened with these reports 👇

INTU had its 2nd consecutive positive earnings reaction:

Intuit rallied 8.1% after this earnings report, and here's why:

The company grew revenues by 15% year-over-year, GAAP operating income by 20%, and GAAP diluted EPS by 19%.

Management increased its full-year outlook across all major metrics, including revenue, operating income, and EPS.

TurboTax Live revenue is expected to grow by 47% this year.

This company is back to growing after several years of stagnation, and the market loves it.

As you can see on the chart, the price recently broke out of a textbook multi-year accumulation pattern.

We think this is the beginning of a brand-new primary uptrend.

If INTU is above 717, the path of least resistance will likely remain higher for the foreseeable future.

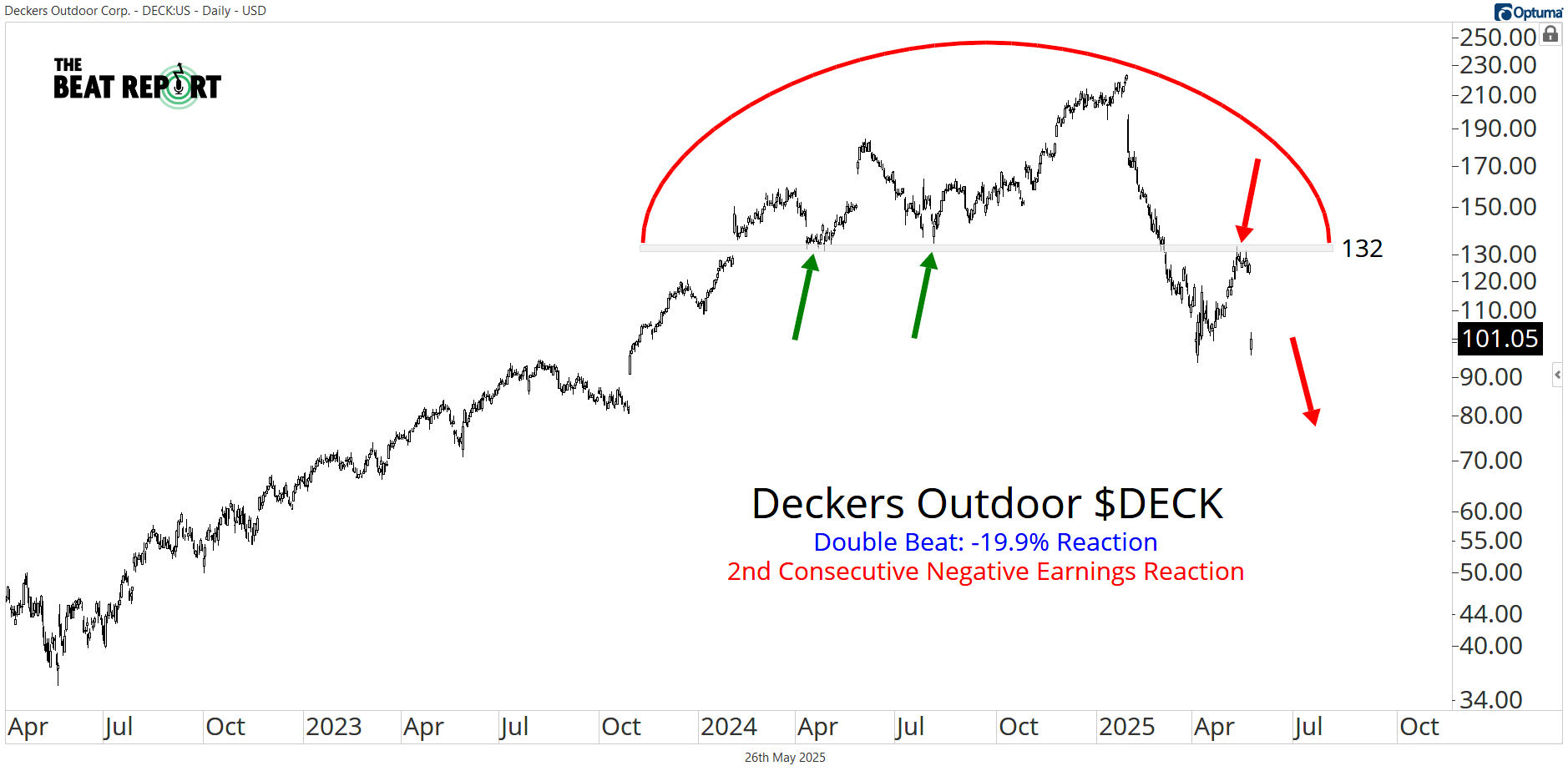

DECK had its 2nd consecutive negative earnings reaction:

Deckers Outdoor fell 19.9% after this earnings report, and here's why:

They expect up to $150 million in increased cost of goods sold in fiscal 2026 from tariffs.

HOKA's U.S. direct-to-consumer (DTC) growth slowed. This has been the major driver of growth for the company.

Management did not provide formal full-year guidance for fiscal 2026 due to macroeconomic uncertainty related to new tariffs and global trade policy. This lack of visibility has spooked the market.

In recent years, this company has been one of the best growth stories in retail, but everything changed after its Q1 2025 earnings report.

It snapped a streak of 5 consecutive positive earnings reactions with its worst reaction since 2012.

Now, this negative fundamental trend is accelerating.

The stock rallied over 500% from its 2022 low to its 2025 peak, but that primary uptrend has ended with the price decisively resolving a textbook distribution pattern.

If DECK is below 132, the path of least resistance will likely remain lower for the foreseeable future.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!