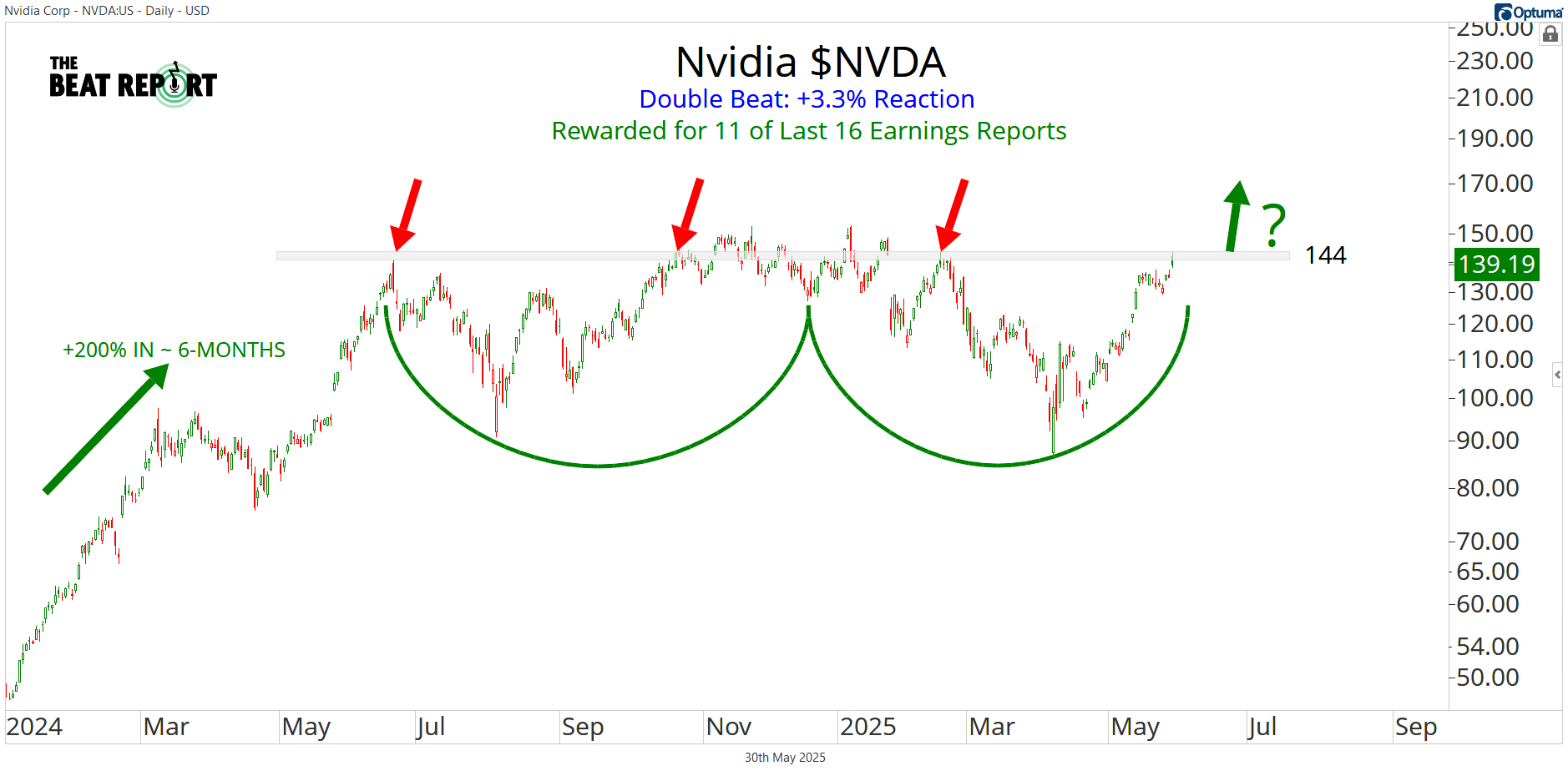

Nvidia $NVDA keeps solidifying its position as the kingmaker of the AI boom, quarter after quarter.

The company just posted another blockbuster earnings report and got rewarded for it.

That marks the 11th positive earnings reaction out of the last 16 quarters. This is one of the best streaks in the market.

The fundamentals are simply stunning.

Profitability isn’t just growing, it’s exploding, and shareholders are making a fortune.

They've become the essential infrastructure provider for the AI economy.

Everyone needs their hardware and software stack, from hyperscalers and cloud providers to sovereign AI projects.

Their CUDA ecosystem and full-stack development model continue to build a wider competitive moat each quarter.

After a brief period where the market failed to reward strong numbers, this latest earnings reaction suggests the appetite for Nvidia exposure is still alive and well.

This isn’t just another tech stock. It's the engine of the AI revolution.

So what else did we learn from yesterday's earnings reactions? Let’s dive into the details.

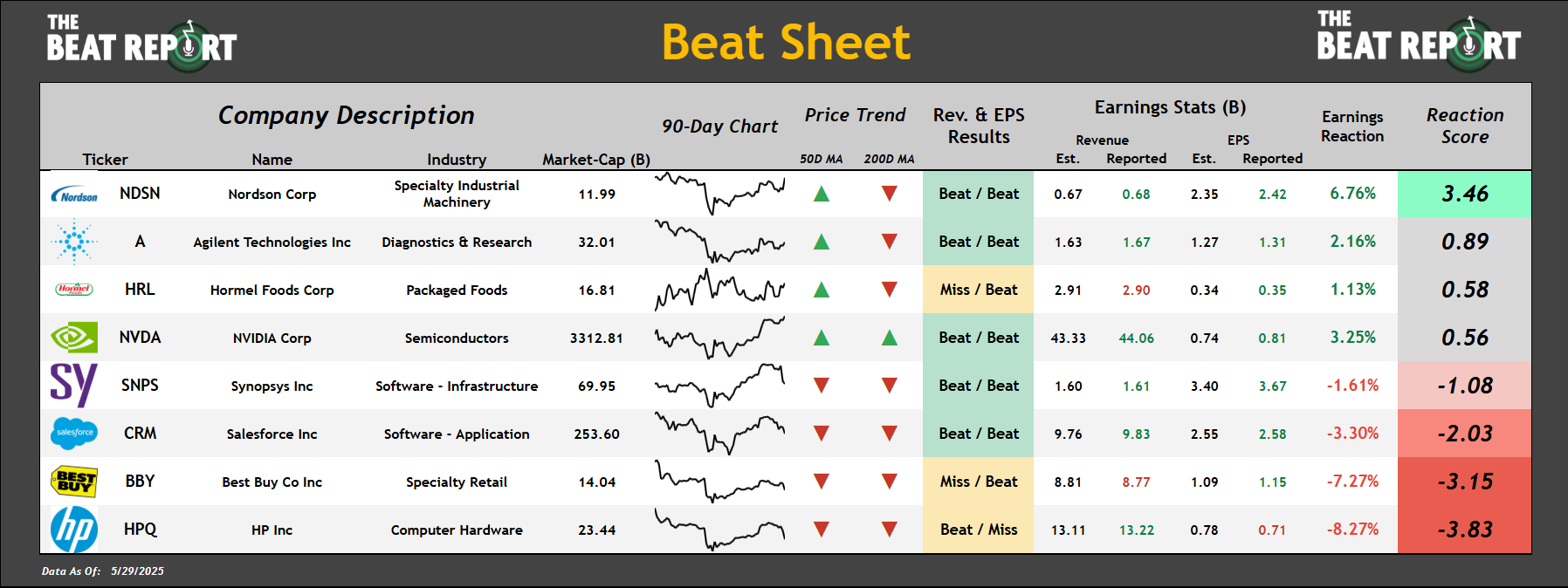

Here are the latest earnings reports from the S&P 500 👇

*Click the image to enlarge it

Nordson $NDSN had the best reaction score after reporting a double beat.

The company reported revenues of $680M, versus the expected $670M, and earnings per share of $2.42, versus the expected $2.35.

HP $HPQ had the worst reaction score after reporting mixed results.

The company reported revenues of $13.22B, versus the $13.11B estimate, and earnings per share of $0.71, versus the expected $0.78.

Now let's dive into the data and talk about what happened with these reports 👇

NVDA has been rewarded for 11 of its last 16 earnings reports:

Nvidia rallied 3.3% after this earnings report, and here's why:

Revenue for the quarter was $44.1B, up 69% year-over-year. This was driven by Data Center revenue, which increased by 73% over the same timeframe.

Despite a $4.5B charge related to U.S. export controls on H20 GPUs shipped to China, gross margin excluding this charge would have reached 71.3%.

The company returned a record amount to shareholders in Q1 through share repurchases ($14.5B) and dividends ($244 million).

This company has been one of the hottest growth stories on Wall Street for years and remains so today.

The consistent positive earnings reactions show that the market loves what this company is doing.

As you can see on the chart, the price is flirting with the resolution of a massive accumulation pattern.

We think the stock is poised to resume its long-term uptrend before long.

If NVDA is above 144, the path of least resistance will shift from sideways to higher for the foreseeable future.

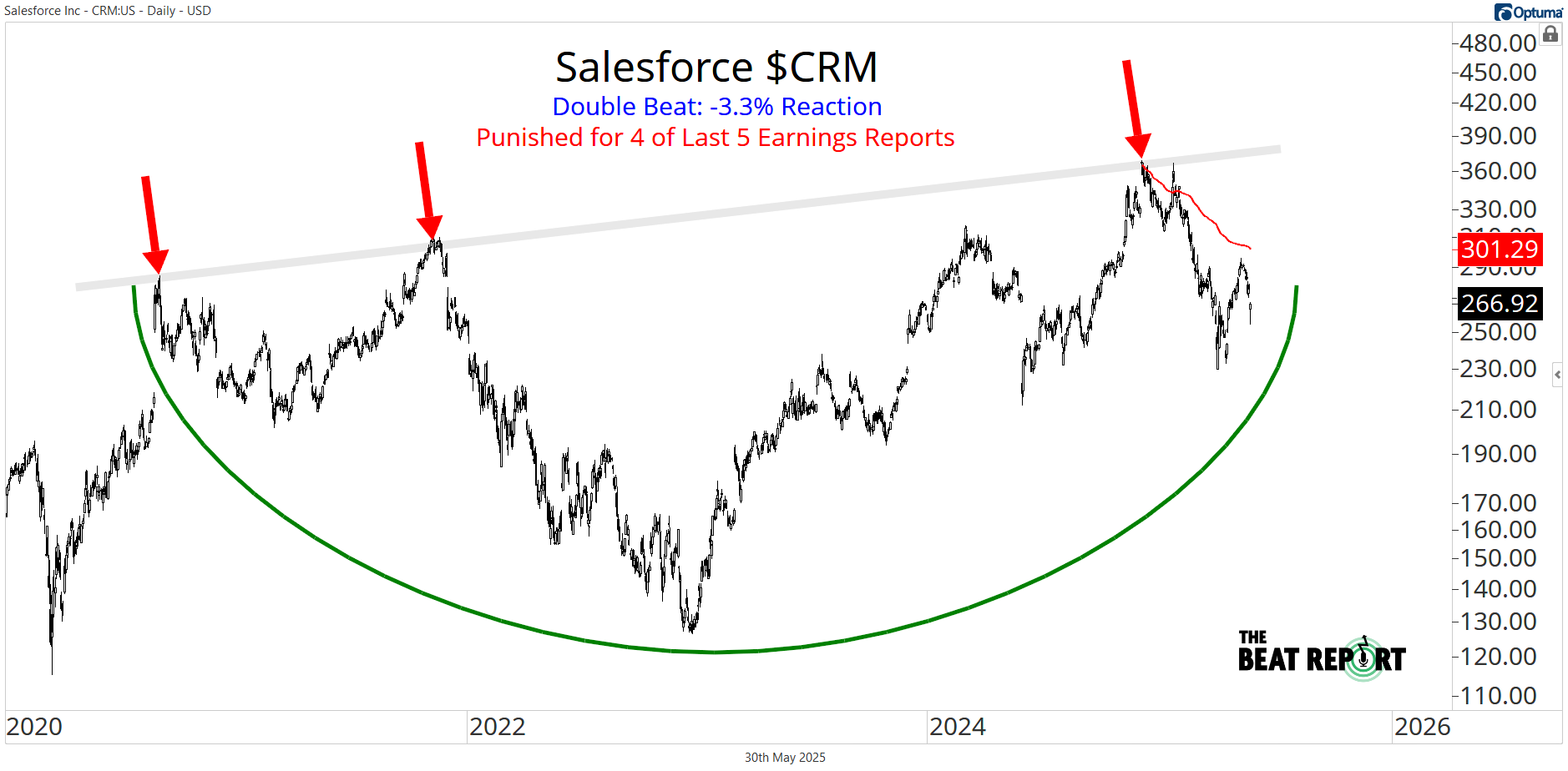

CRM has been punished for 4 of its last 5 earnings reports:

Salesforce fell 3.3% after this earnings report, and here's why:

Overall growth remained modest at 8% year-over-year.

Several core business areas showed concerning trends:

Sales Cloud growth slowed to 7% Y/Y.

Service Cloud also decelerated to 7% Y/Y.

Marketing and Commerce growth was weak at just 4% Y/Y

Professional services revenue declined 3% Y/Y

The company plans to hire 1,000 to 2,000 more salespeopleand expand distribution capacity by 22% overall. This is likely to pressure margins in the future.

This company is one of the largest in the Software industry, but it's not growing like it was years ago. That's why the market assigned it a much lower earnings multiple than many of its peers.

As you can see on the chart, the price action has been incredibly messy for years, and we don't anticipate that changing soon.

If CRM is below 301, the path of least resistance will likely remain sideways for the foreseeable future. The VWAP anchored to the all-time high is our line in the sand.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!