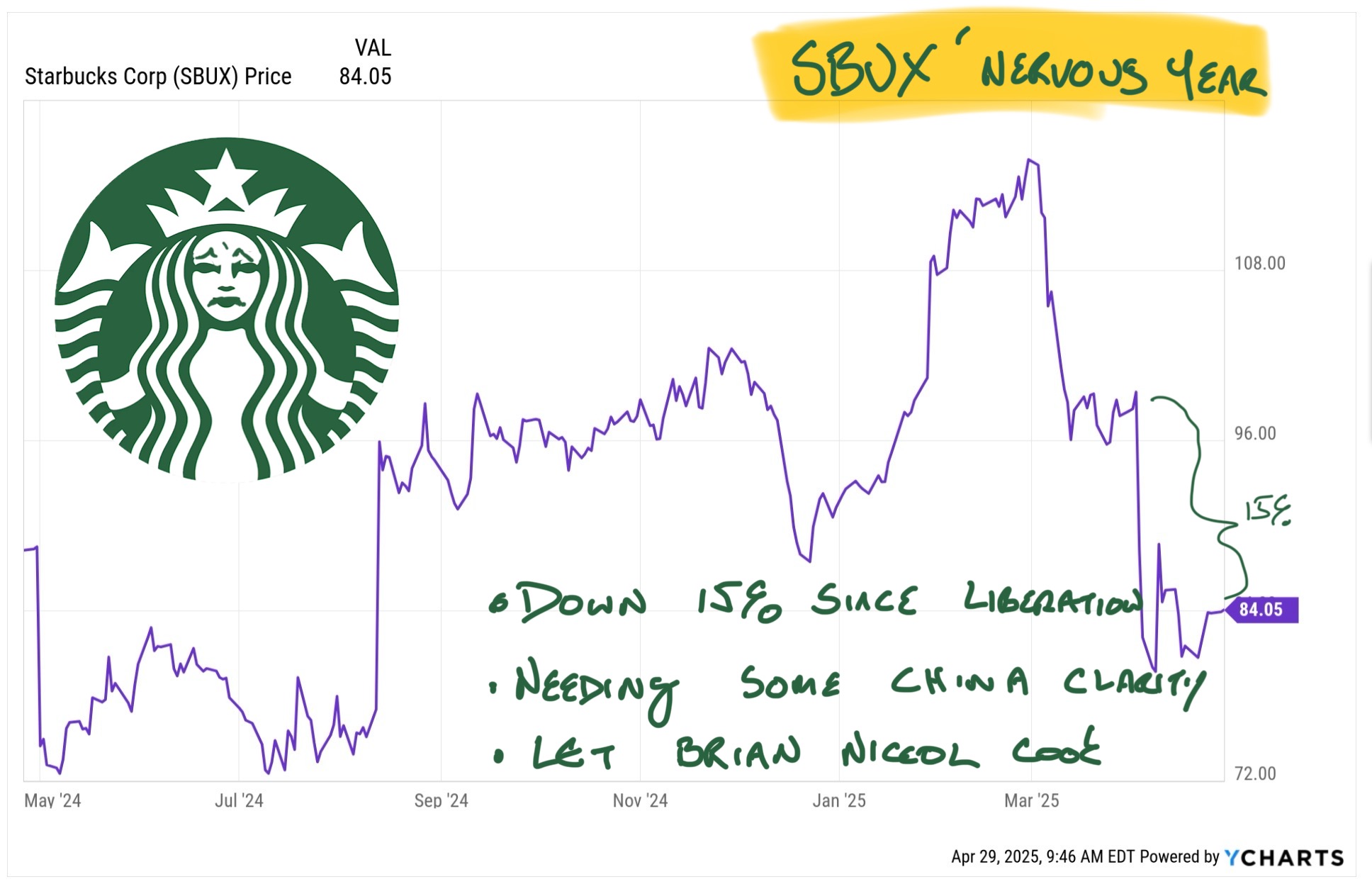

Starbucks set to report tonight and if you aren't nervous you haven't been paying attention.

Shares of the worlds largest coffee shop are trading at levels first hit in 2019, a depressing run of mediocrity that has included 4 CEOs, a national controversy over the use of store bathrooms and the COVID lockdown. The lockdowns were particularly notable for Starbucks because ~20% of its revenues (and much less of its earnings) are generated in the Chinese market, which was something of a career-long hobbyhorse of longtime leader Howard Schultz.

The company pulled all guidance last fall, one of the first orders of business under CEO Brian Niccol. Suffice it to say the business outlook hasn't gotten more transparent since October.

Same store sales were likely down in the US last quarter, though likely with improved tickets but weaker traffic. FWIW analysts are looking for EPS of 50c on about $8.8b of revenue. There will be currency noise and, as just mentioned, Starbucks itself isn't giving any guidance and has no particular incentive to stretch numbers or paint a rosy international picture. Niccol arrived with a well-earned reputation and he's delivered so far but he's never pretended to be omniscient.

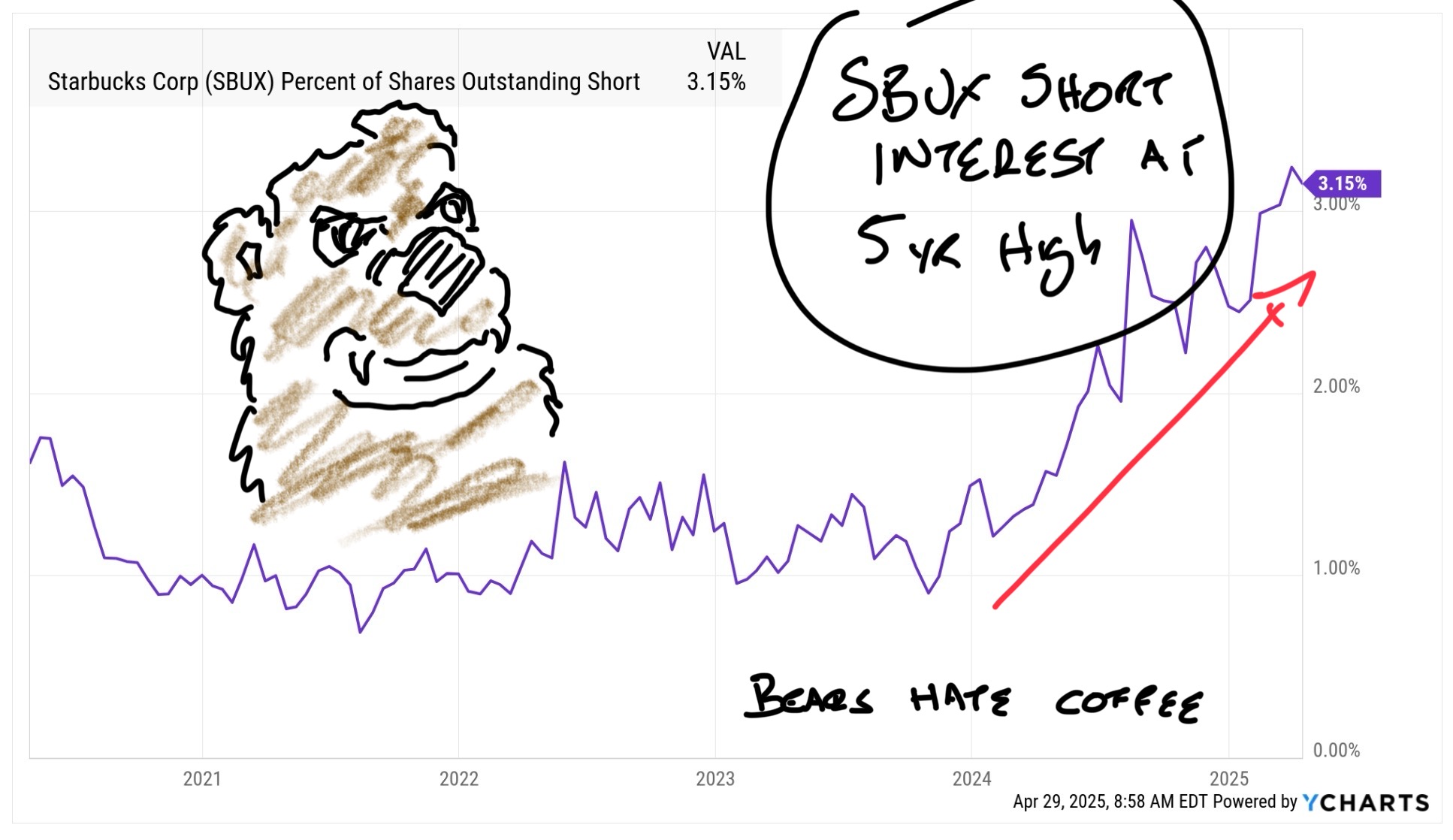

That's the bad news. It's not a secret, which is why short interest has gone up 3 fold since last year and sits at 5 year highs:

The Bullish Case Ahead of Earnings

All of which makes for a solid case for betting against Starbucks here and now. Here's what I wrote about the company in March:

"Starbucks (Long $98 )

I've written about Starbucks before and talked about it endlessly. In short: Brian Niccol is putting together exactly the turnaround Starbucks needs right now. Simple. Focused on customers. Measurable performance indicators rather than a reliance on surveys and app sign-ups.

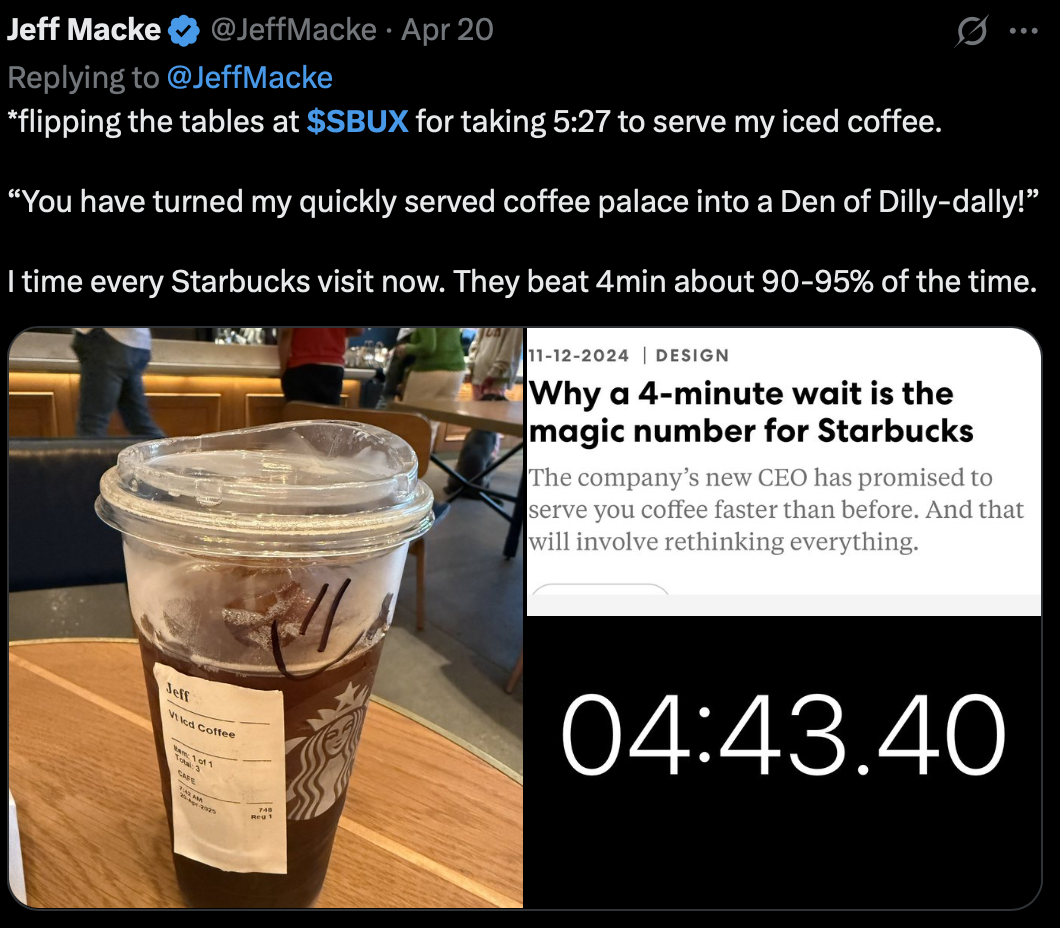

When you walk into a Starbucks you can expect your drink no more than exactly 4 minutes from the time you place your order.

Every associate in all 40,000 Starbucks is aware of this rule or will be very shortly. A fast, accurate order every time fixes about 90% of the things people think they hate about Starbucks.

"4 minutes" is the conversation at Starbucks now. That's just so much better than Unions and junkies in the bathrooms."

Since then I've been to a few dozen Starbucks, from San Diego to Texas to Maryland and New York. It's honestly much more coffee than I need. But the US units are the key to any long bet on Starbucks. If Niccol can't improve the customer experience nothing else will matter, at least for the stock.

I think Niccol is a change agent. I know Starbucks can, and is, improving in stores. How do I know? Because like all good leaders Niccol and co have told us the exact metric he's demanding from stores: 4 minutes from order to delivery.

There's more to the story. The company has simplified the food selections (and improved the quality, tightened up the coffee options, and stepped slightly back from efforts to create Instagram-friendly colorful drinks for kids that take 10 minutes to make at the expense of enraging core customers.

But for mystery shopping purposes 4 minutes is a measurable in-store goal any customer can track. Which is exactly what I've been doing, all over the country. Here I am enjoying Annapolis:

Starbucks isn't perfect but they're at about 85% in my travels. And the stores are cleaner. The workflow is tighter. The stores are more efficient.

And the Annapolis store only missed one time in 4 days. Pretty good for a college town.

Starbucks has 20,000 stores all over the world. They do nearly $30b a year in coffee sales just in the US. Despite all the FX headwinds, the China issues, and pressure on the consumer, if Starbucks can keep improving the store experience the customers will come. There's a lot of room for improvement.

What I'm Watching for Earnings:

Back to Starbucks Progress

Comps are likely to be soft but in this very particular global situation, I'm willing to give the company a bit of a pass. What I do want to see is continued progress on execution. I'm good with more money being spent on the domestic stores. These are "soft metrics" but 20,000 unit operations turn like battleships. They need some space and time. It's been over a decade since Starbucks paid this much attention to the store experience. This effort deserves runway.

China Update

I'm not expecting good news or strong comps out of China. There is existing chatter of a backlash against US companies in the nation (can't understand why) which could impact comps, as will economic set-backs. Thus far Niccol has been relatively quiet about the plan for China. Starbucks has a huge investment and not a great deal to show for it beyond the top line. Deemphasizing China, even suggesting some sort of reduction in the footprint would be welcome by me, if not most investors.

Street Reaction

So far CMG and other QSR names have reported soft SSS and gotten away with it more or less unscathed. Going into the report tonight, when bad numbers are all but assumed, the movement of the stock will reflect confidence (or lack of same) in managements plan more than whatever metric the headlines claim.

Trading Plan:

Starbucks is an investment, not a suicide pact. I don't have endless patience but now that the post Niccol stock price spike from the announcement of Niccol jumping to SBUX from CMG I'm not inclined to get shaken out now. I'm grading Starbucks on the above criteria. If the company performs I'm comfortable with more near term pain. I think the lever to be gained in US and non-China locations is more than enough to pay off (as always, "assuming the entire globe isn't plunged in to a global depression")