On Holdings, Cava and Birkenstocks are poised to move this week.

August 10, 2025

According to Deutsche over 60% of the consumer facing companies that have reported so Q2 so far are lower. What's striking / concerning / disturbing is the spread between winners and losers. The downside reactions (RIP $CROX) are brutal, the upside ($BROS!) mostly limited.

There's still a week to go before Big Daddy Walmart reports but that doesn't mean we don't have plenty to do over the next 5 days. Here's a quick look at 3 names with a lot on the line when reporting this week:

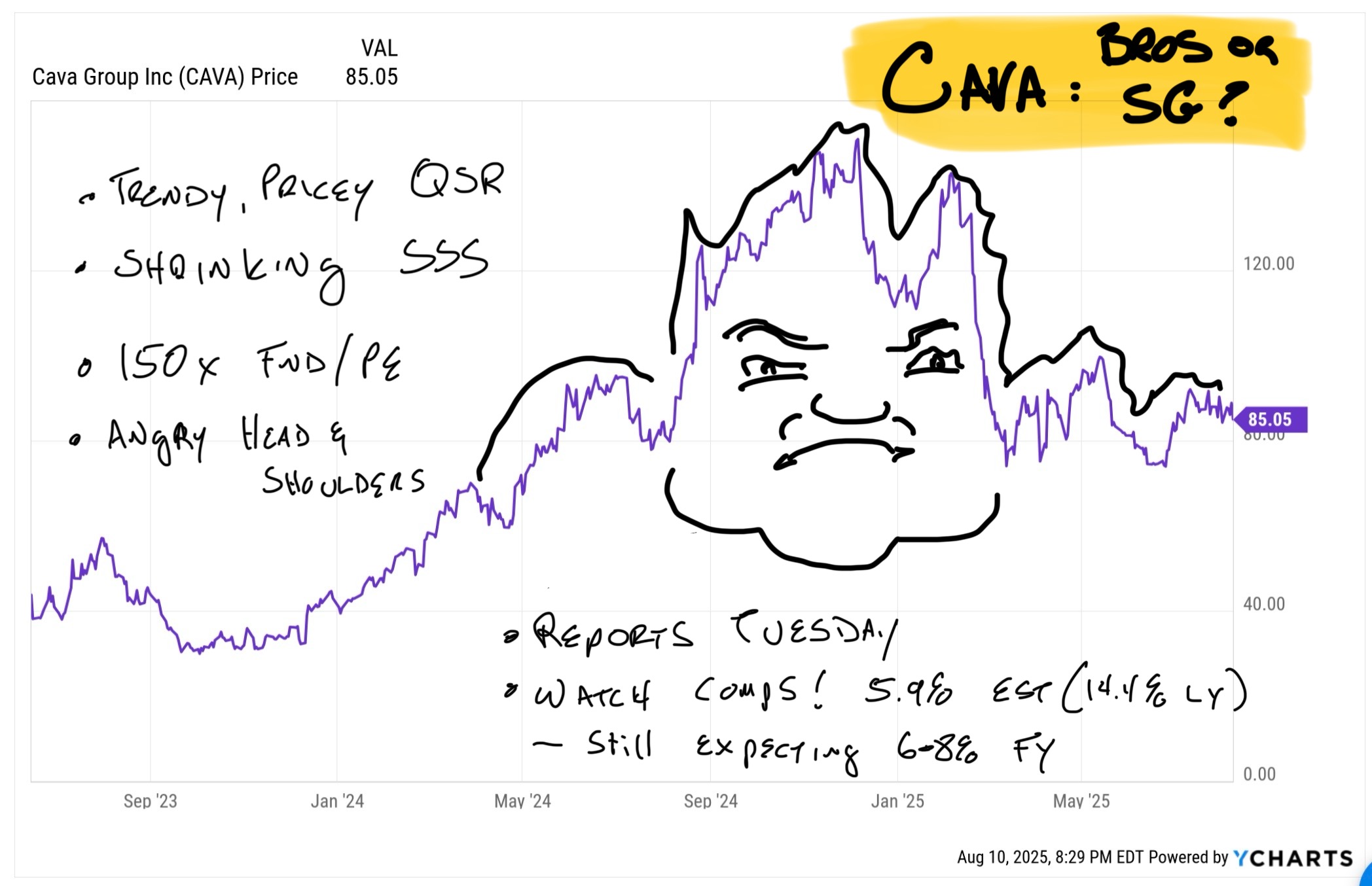

CAVA: $85.05, Reporting Tuesday

Pricey, trendy Mediterranean QSR with shrinking comps. Suffice it to say the results from Cava's space haven't been "overwhelming" so far. Company reports Tuesday. I'm watching comp store sales which are expected to come in at 5.9% for the Q and 6-8% for the FY.

That latter number is in danger.

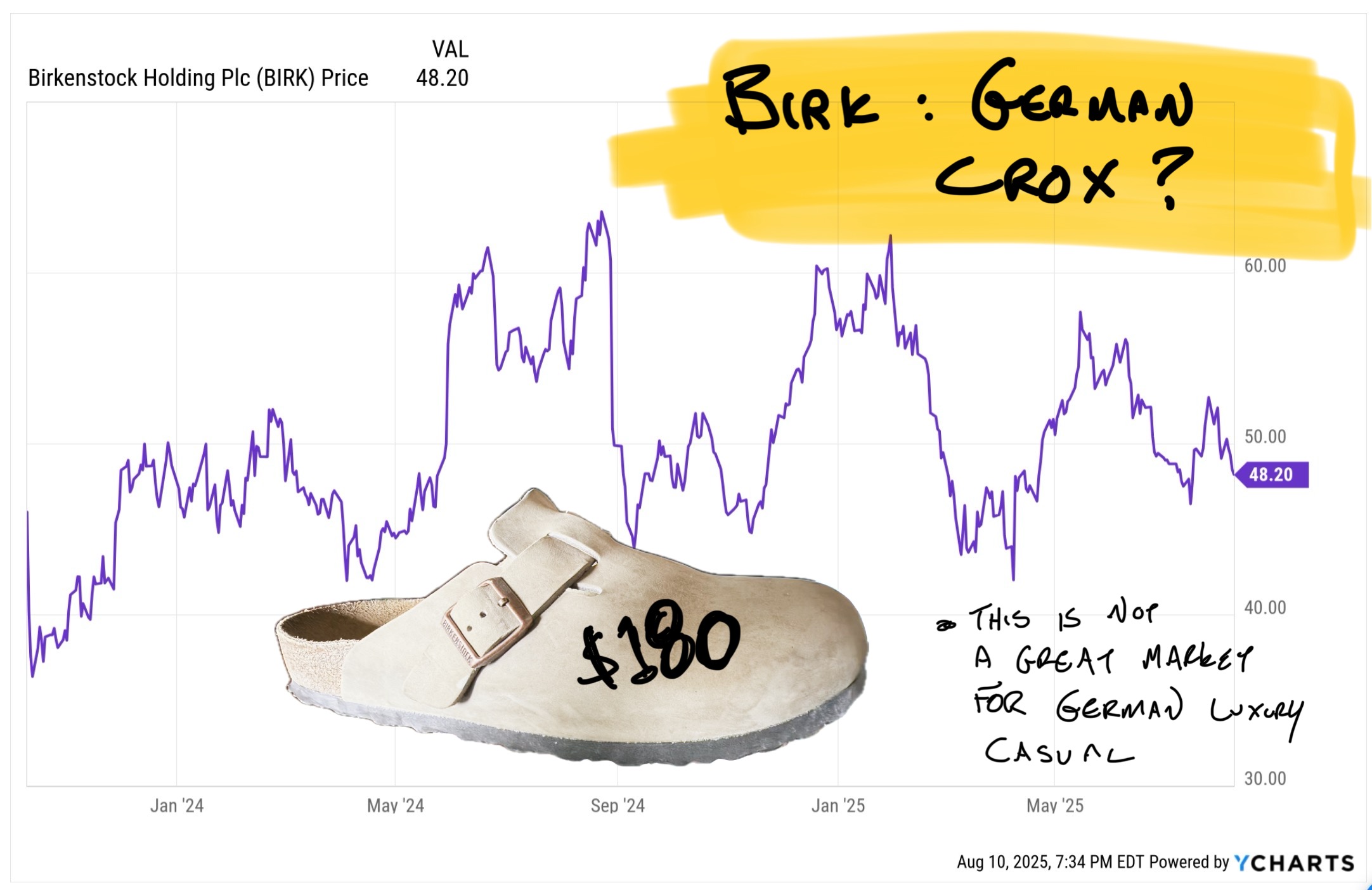

Birkenstock $48.20 Thursday Morning

We've got 2 European shoe makers this week. They've got different stories and long term potential but the headwinds are the same: Expensive Product, Tariff Exposure, Not Cheap.

Thursday brings us Birkenstock, the 250 year old German hippy shoe maker. Honestly, I'd normally not pay that much attention to BIRK but the company has held in better than I'd expected and my son, who is the sort of "accidentally trendy" consumer worth watching showed up with a $180 pair of Birks just last week.

He loves them and makes his own money... so there wasn't much I could do to object. But this seems like a brutal market to be selling expensive, foreign, leather flip flops. If the market can kill Crocs for 30% and destroy Deckers and kill luxury in general (with a few exceptions) there's a lot of air-pocket risk for Birk.

ON Holdings: Tuesday Morning

I love specialty retailers taking share. I feel very strongly that ONON is crushing Lululemon and just about everyone else when it comes to share.

But everything I said about Birkenstock applies to ONON, only more so. On has more variability, higher expectations and all the exposure of Birk.

The agonizing thing is, in a better environment, On would be the kind of stock you hold for a long time and ride it out. I made 10x with Lulu using that strategy and it could apply here.

But "could" is doing a lot of heavy lifting. On is expected to grow over 40%. The company blew out expectations last quarter and has given back every penny and then some since May.

There just isn't much ONON can say that's going to lead to a sustainable rally. Every trade policy change impacts On's insanely fat margins. I'd love to buy the stock back lower and I suspect I'll get a shot. If not this week, probably later this year.