Nike reports tonight. Here's how they got into this mess.

By Jeff Macke

September 30, 2025

Nike's investor relations homepage features a Mission Statement that all but screams written by committee. “Nike, Inc. is a Growth Company,” it declares, “We create innovative, must-have products. We build deep, personal connections with consumers. And we deliver an integrated marketplace with compelling retail experiences.”

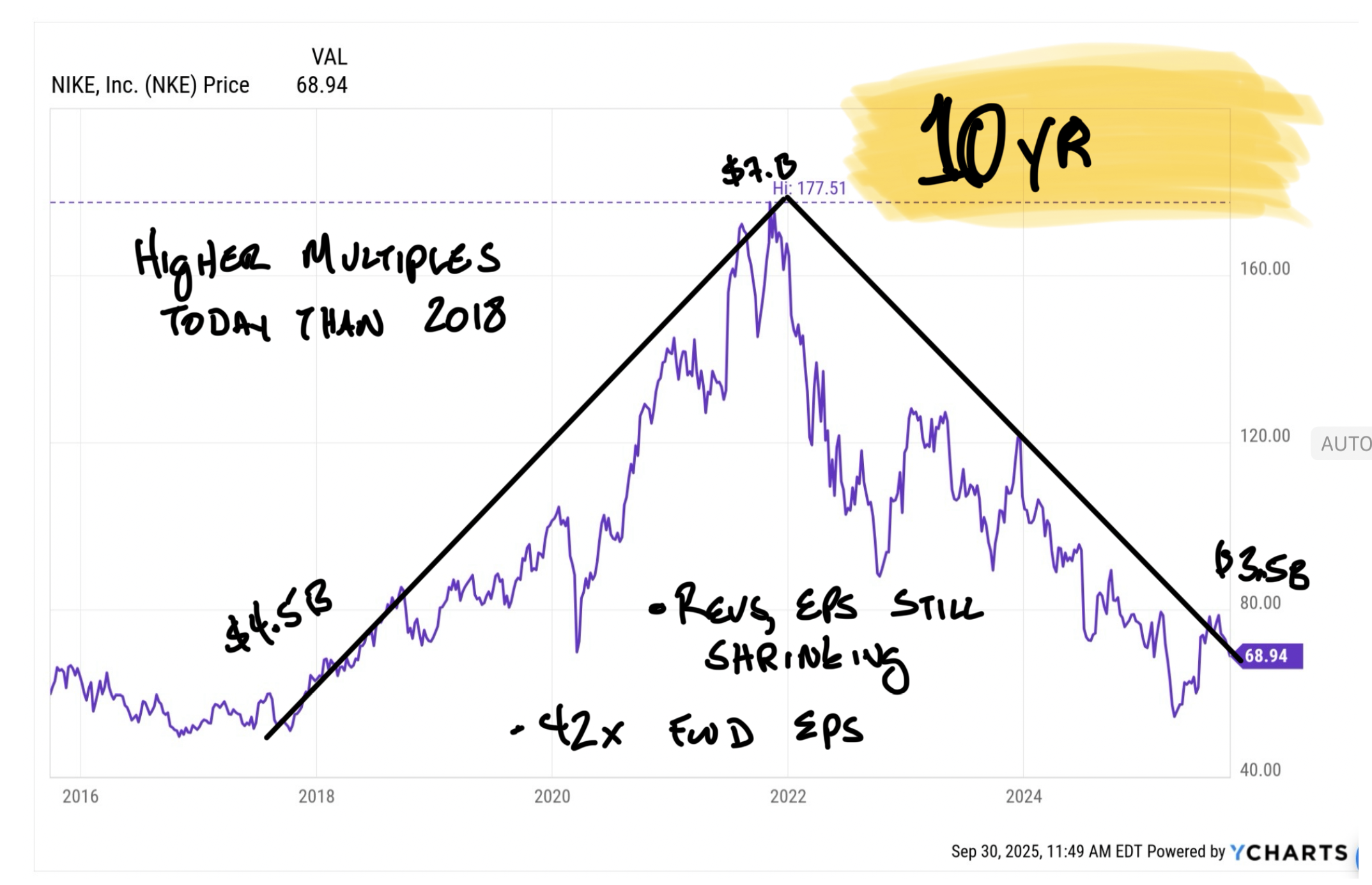

Nike’s statement is not just wordy; it hasn’t been true for years. Nike doesn’t make must-have products, struggles at physical retail, and, most notably, isn’t a growth company. Margins, EPS, and now revenues are shrinking. Nike is going to earn about a billion dollars less than it did during this same quarter in 2018. That's not what growth looks like.

Nike is expected to report earnings per share (EPS) of $0.27 this quarter, compared to $0.66 for the same quarter last year. Revenue is projected to decline by approximately 5% year-over-year to around $11 billion. Gross margins are expected to fall by 350 to 425 basis points, largely due to tariffs that Nike is unable to offset. These declines suggest ongoing financial challenges.

There’s plenty of blame to be attributed to Nike’s current state as a business and a stock. Most notably, Nike shouldn’t have cut out smaller retailers to push Nike Direct to Consumer. The plan was to control its brand and boost prestige by selling only where it could control the experience. In practice, Nike is successful online, but it has struggled to make its physical stores profitable, failing to offset the losses of jilted merchants. When Nike dropped vendors, stores started selling Hoka’s and On shoes—brands that did well in large part by not being Nike.

Nike’s new CEO is attempting to reverse these setbacks, but improvement will take time. If Nike shares were inexpensive, this might not matter as much, but that’s not the case: Nike’s stock currently trades at 42 times expected earnings. For comparison, On Holding ($ONON), an actual growth company that makes innovative products people love, trades just over 50 times. I’d honestly rather bet on the Swiss.

The Trade

I know this is a familiar argument. No one really likes Nike now unless making a flashy Contrarian call. That’s fine. Nike could still rally tonight.

If revenues get within 1% of flat (possible), the stock could bump to $80. If that happens, we finally have a trade: Short Nike at $80. For patient contrarians, Under Armour is a better play. UA shares problems, trades at lower multiples, and has more entertaining conference calls.

More:

I find Nike a fascinating disaster. It was fun going back to read how hyped the move was at the time and how quickly it became a Harvard Business School case study of what not to do.