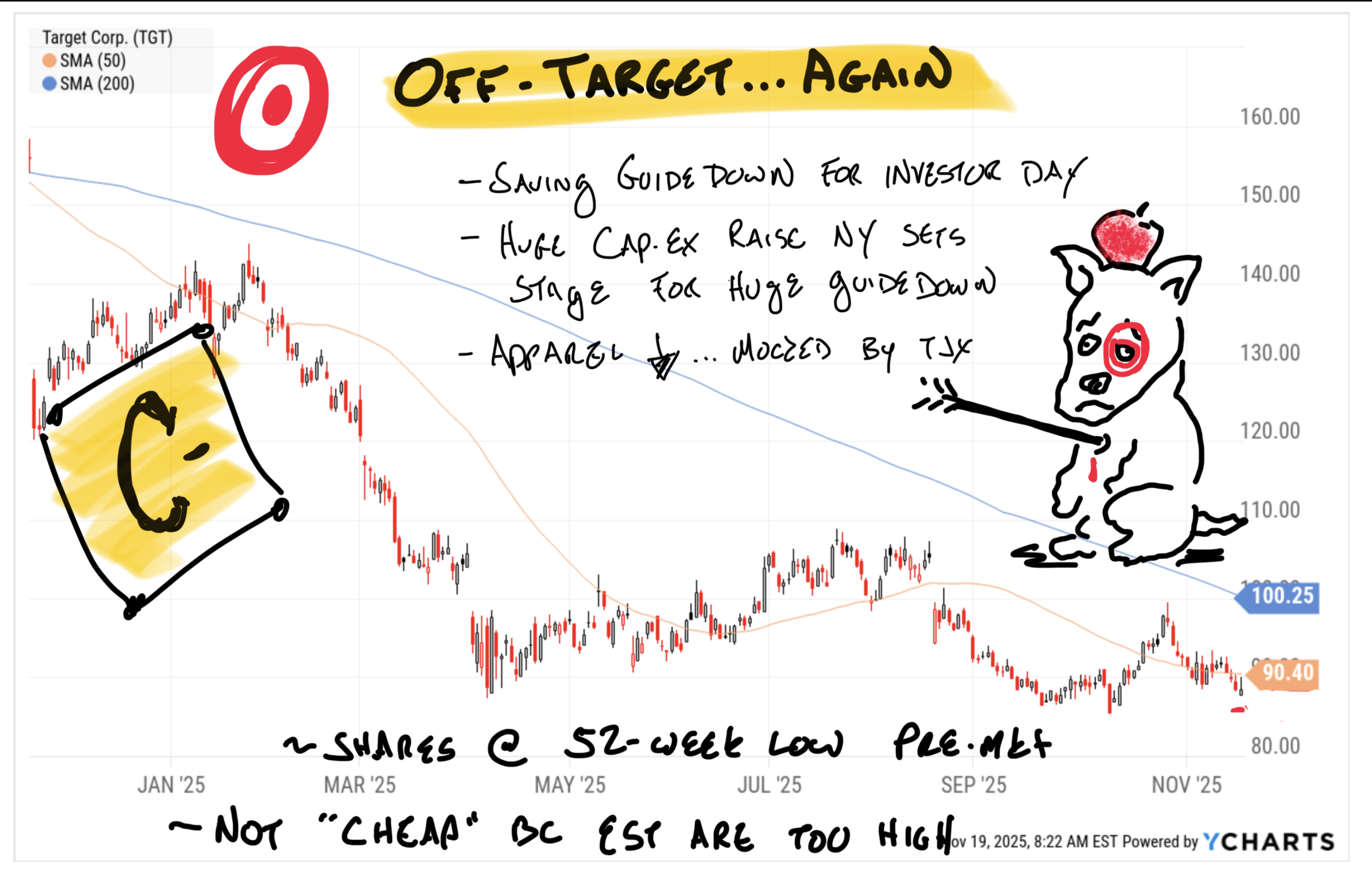

The retailers reported about as expected this morning. The good stores beat and guided to a decent Q4. Target mentioned consumer sentiment a few times, guided revenue lower, and announced a huge capex expansion for next year, suggesting estimates will come way down when Target reports Q4 in February or March.

Building on those results, Christmas is also shaping up to meet expectations, according to today's reports. It won't be spectacular, but it won't be disappointing either, and might even turn out to be the Best Christmas Ever in terms of total sales.

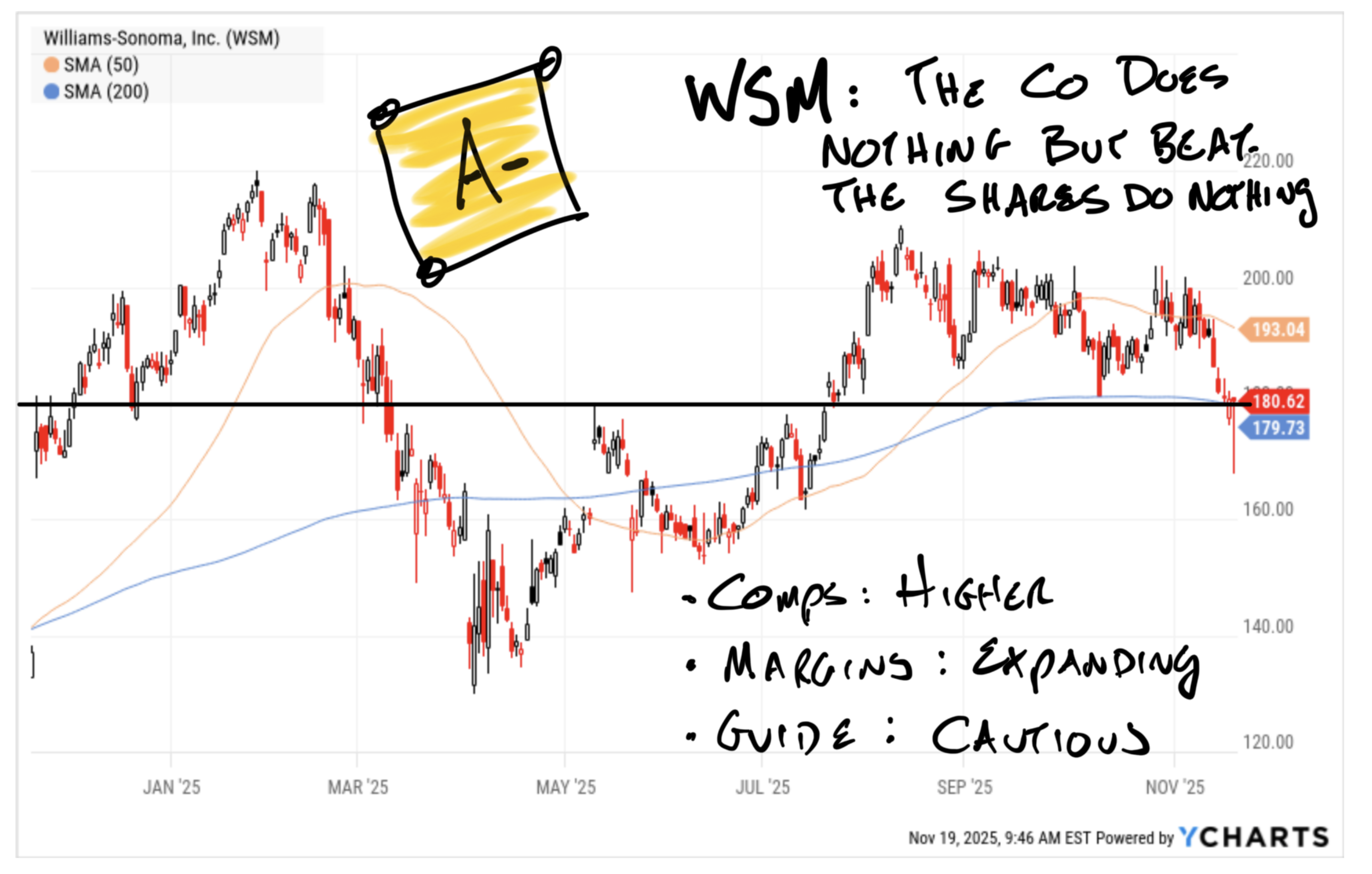

TJX and WSM both outperform on comps and margins, suggesting shoppers are still showing up for what they want. WSM doesn’t run deep discounts or compete on price. In a truly strapped economic world, WSM wouldn’t beat.

During its 60-minute report, Target mentioned strength in toys and denim. The latter bodes well for Gap, which reports Thursday.

On to the Report Cards:

Target: C-

Hit the EPS number. Margins falling despite 90bps tailwind from shrink recovery. Same-store sales and transactions are both lower again. Target would be better off unlocking the product at the expense of more theft if it meant that paying customers could find it.

Translating from retail-speak, Target is still getting worse. New management plans to increase CapEx by 25% next year, bringing the total to $1b. As a low cash-flow operation, this means at least 2 things for next year. First, estimates are way too high for EPS and next year's sales. Second, F27 is make-or-break for Target. The balance sheet is fine, for now, but at 3.4% operating margins, Target better deploy that CapEx productively.

If the additional spend doesn’t lead to improved performance almost immediately, Target will be a “cash-strapped merchant” in short order.

With this in mind, expect Target's Q4 report in February to include guidance well below the ~$8 EPS target for next year.

TJX: A

TJX is drinking Target’s Milkshake.

Performance metrics further support this: TJX is seeing comps rise across the board and is raising its outlook. By tapping into the challenged consumer—selling off-price goods—TJX capitalises on market needs. Despite similar business models, TJX consistently outperforms Target in understanding and serving its customers.

Which is why TJX is beating Target in the marketplace and the stock market.

TJX beat on comps, raised guidance, and continues to have the clearest messaging in the industry. Let’s just let the CEO explain it:

“Ernie Herrman, Chief Executive Officer and President of The TJX Companies, Inc., stated, “I am extremely pleased with our third quarter performance and the excellent execution of our off-price business model by our teams across the Company. Sales, pretax profit margin, and earnings per share all exceeded our expectations. Overall comp sales grew 5%, with strength across every division. We believe this is a testament to our value proposition and treasure-hunt shopping experience, which continue to draw consumers to our retail banners worldwide.”

Tattoo it right on my back.

Williams-Sonoma: A-

I’m a huge, unabashed fan of WSM CEO Laura Alber. The company beat across the board, expanding margins and posting 4% comp store sales. As feared (and why I sold the stock for the Portfolio+), guidance was cautious, essentially because what the hell else is a company selling housewares and furniture imported from around the world (including China) going to say?

WSM has beaten its quarterly results every quarter this year. In a less complicated environment, shares would be about $250. In America, the stock is slightly lower in early trading and is likely to settle about flat. (note: It’s already flat as I type at about 7am)