Mattel Takes it on the Chin in the New World of Toys

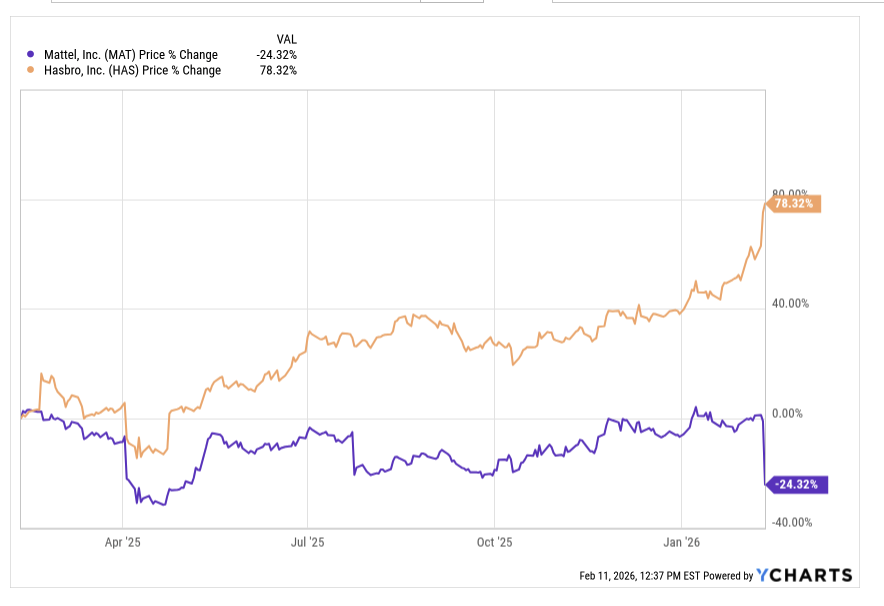

The Q4 2025 earnings results for Mattel and Hasbro have revealed a significant strategic divergence. While both companies faced a "just-in-time" holiday ordering shift from retailers, Hasbro’s digital fortress allowed it to withstand the blow, while Mattel’s inventory-heavy model led to its worst stock plunge in decades.

Inventory & The Retailer "Risk-Shift"

In late 2025, major retailers like Walmart and Target successfully shifted the risk of unsold toys back onto the manufacturers. By delaying holiday orders until late September and opting for domestic shipping over direct imports, they forced toymakers to act as warehouses.

Mattel’s Struggle: Mattel ended the year with $827 million in inventory—a 12% increase—much of which arrived too late for the holiday peak. This "inventory pile-up" was the primary driver of a 480-basis-point drop in adjusted gross margins. CEO Ynon Kreiz admitted that while consumer demand was decent, retailers focused on clearing their own shelves rather than placing fresh orders for Mattel's core brands.

Hasbro’s Mitigation: Hasbro managed to keep its inventory more lean, ending the year at roughly $417 million. Because they had already "rationalized" their product lines (cutting unprofitable SKUs), they were less exposed to the retailer destocking trend that hammered Mattel’s Fisher-Price and Barbie lines.

Tariff Exposure & Margin Lags

Both companies are grappling with the "timing lag" of newly implemented tariffs on goods from China and Vietnam.

Mattel: Reported that tariff costs hit margins harder than expected in Q4 because their "mitigating actions" (like price hikes) won't fully take effect until mid-2026.

Hasbro: Modeled a $60 million tariff impact for 2025, with costs expected to rise to $100M+ in 2026. However, Hasbro’s supply chain is more diversified; they aim to have less than 30% of their U.S. revenue sourced from China by the end of 2026, compared to Mattel’s slower exit.

The Digital Divide

The most striking difference is the 2026 outlook.

Hasbro (The Winner): Despite a "cloudy" toy market, Hasbro shares rose 9% because its Wizards of the Coast (Magic: The Gathering) and digital gaming segment grew 44%. This high-margin "digital buffer" protected their bottom line.

Mattel (The Warning): Mattel is only just beginning a $150 million digital pivot to buy back its mobile gaming joint venture. Analysts noted this investment is "seven years behind Hasbro," and with 2026 EPS guidance of $1.18–$1.30 (well below the $1.75 consensus), investors are treating Mattel as a legacy manufacturer rather than a modern IP powerhouse.

Bottom Line: Toys are a Tough Game

The real winner here, if there is one, has to the be retailers who have managed to push inventory and markdown risk to the toy companies instead of carrying the product themselves. Yet another unexpected turn of events stemming from Tariffs.

Check out my conversation with Spencer for thoughts and let me know what you think.