Nike beat expectations on the top and bottom lines but cautioned the “Holiday Quarter” (Nike’s Q2) would be slightly weaker than analyst estimates. In yesterday’s preview, I suggested revenues could beat estimates and come in “within 1% of flat”. Reported revenue was +1% as reported and -1% in constant currency. Compared to John Donahoe, CEO, Elliott Hill is already demonstrating stronger leadership and decision-making in the role.

All of those are good things. And I still don’t like the stock. Or hate it. I can always change my mind later.

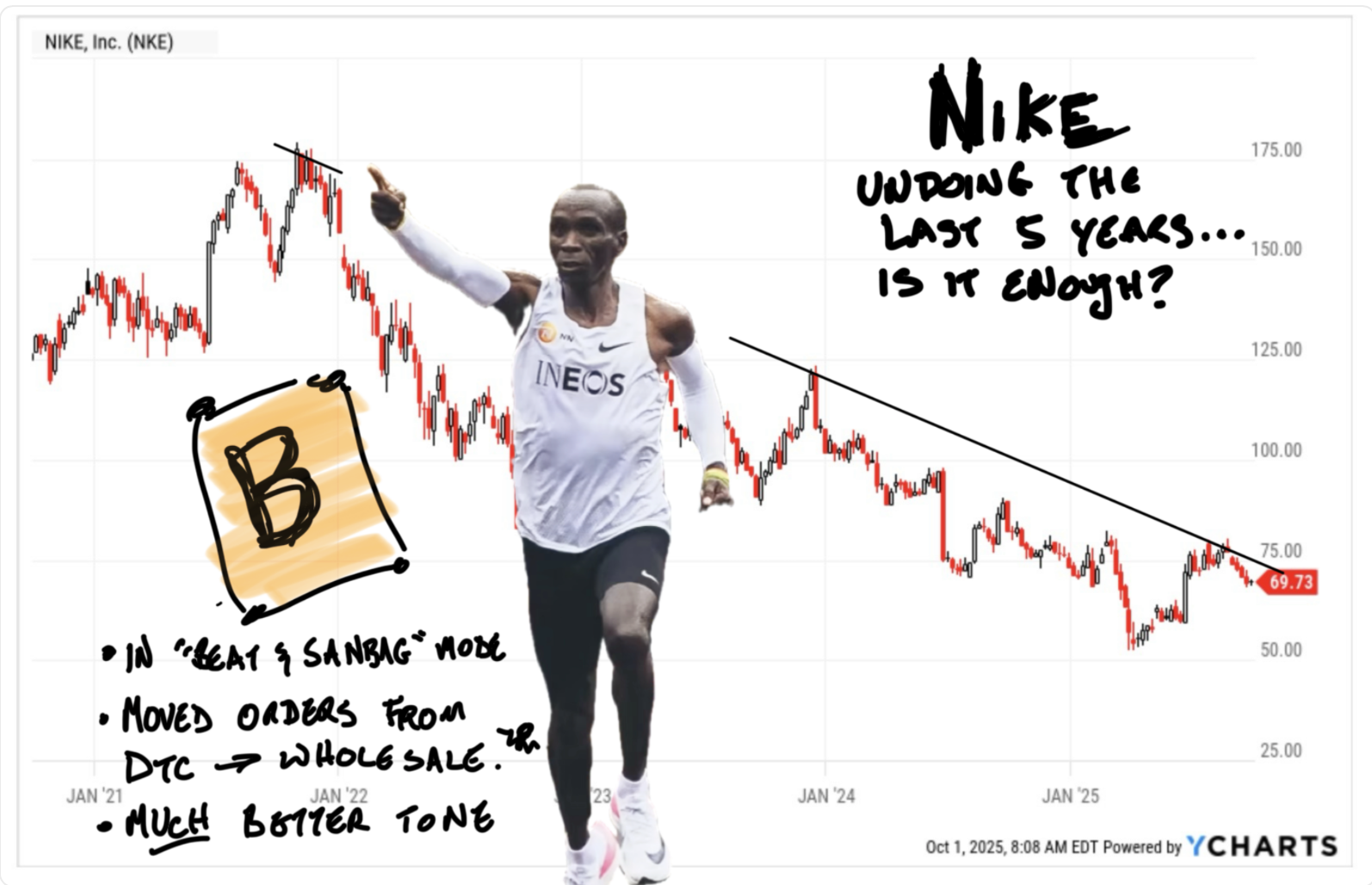

That’s why I grade the quarters. To keep track of progress. So let’s grade Nike:

Financials: B

Yesterday, I discussed Nike reversing its 5-year strategy shift from wholesale to DTC. Last quarter, wholesale rose 7% while DTC dropped 12%. Hill is winning back retailers, but shifting revenue from a profitable channel is no major win.

Apparel surprised to the upside. All markets except America underperformed. The spring order book looks promising. “Innovation” was emphasized.

Narrative: A-

People want to own Nike. It’s easy to imagine a broker convincing slow-money clients to start buying Nike. “You gotta own these giants when no one believes,” they say, probably through thick cigar smoke in a Long Island bucket shop. “Smart money guys like you are loading the boat”. Of course, bucket shops, brokers, and slow-money clients no longer have the same level of firepower they once did.

Nike’s story will improve when earnings and margins stop falling, not just slowing their decline. Blue Chips must need a clear road to Growth. Nike knows the rules.

Final Grade: B

Nike isn’t the short it once was. Elliott is motivated, having been passed over for Donahoe’s failed tenure. If shares had bounced to $80, I’d get short. 4-5% seems fair enough. It means the weak guidance is more about sandbagging than genuine concern. Nothing too exciting. I’m noting the strength in the US and apparel, as well as the weakness in China, and turning to other opportunities.

The Bottom? (Naaah...)

More:

I find Nike a fascinating disaster. It was fun going back to read how hyped the move was at the time and how quickly it became a Harvard Business School case study of what not to do.