We’re at a strange spot in the earnings cycle for merchants. The banks, Mag7 and enough consumer-facing companies have reported. Against all odds, or certainly contrary to conventional wisdom at the end of March, the consumer seems fine. Not great, to be sure, but well enough to eliminate any tangible angst that the retailers are going to announce a collapse in demand in two weeks when we start hearing from Walmart, Target and the mall stores.

Why Gas Stopped Mattering (as much)

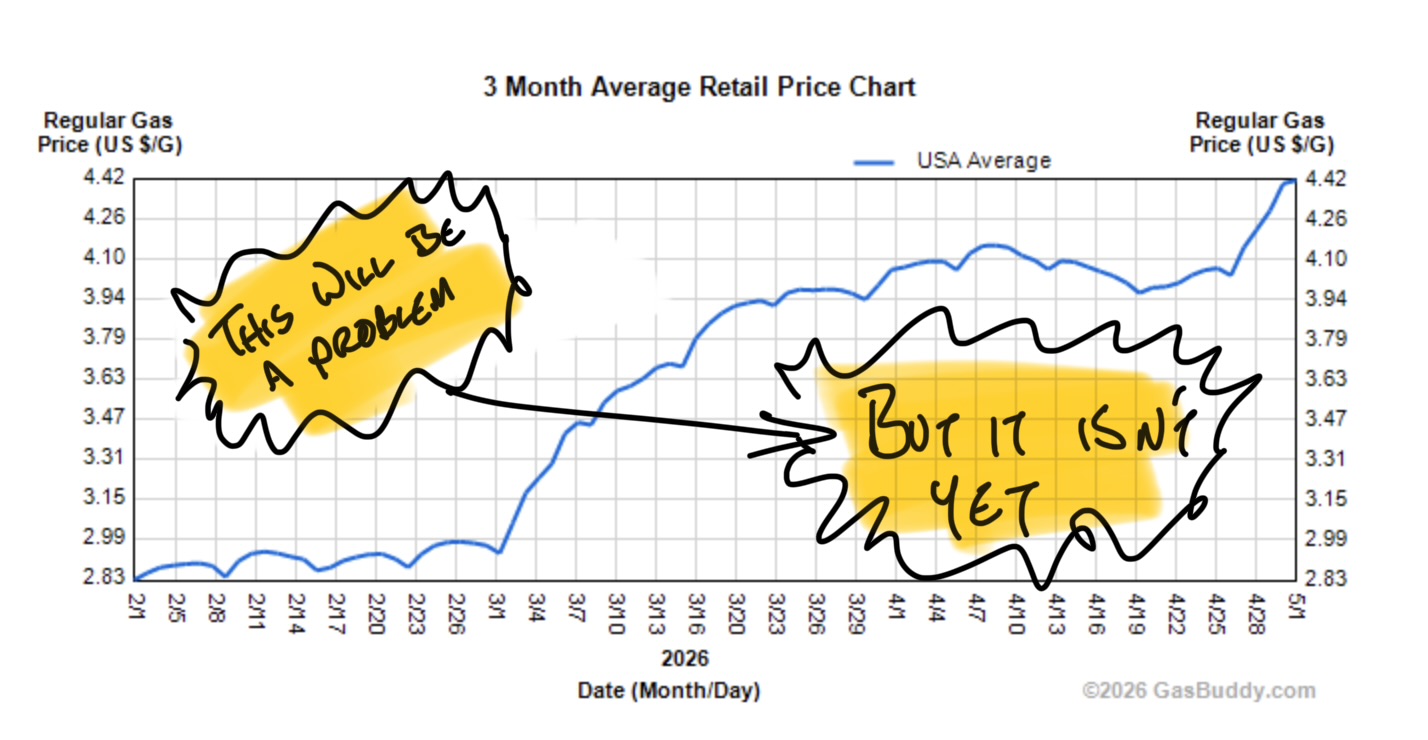

The above chart of gas prices shouldn’t be “great”. It’s the 3 month average price of gas in America. Gas prices have gone up about 50% since the war in Iran started. During March that relationship led to absolute carnage in almost every consumer company you can name. Airlines, mall stores, cruise ships, pretty much anything.

You can make the relationship as complicated as you want in terms of the relationship between crude and global wealth. I like to keep it simple. When gas prices are going parabolic, it costs companies more to sell stuff and people buy less of it. That’s bad for stocks.

So, that part at the upper right of my gas chart, where the price/ gallon has started moving higher again, should be bad. Stocks got smoked in March on gas and once prices finally started pulling back in April consumer stocks ripped higher. So why hasn’t the resumption of the uptrend of gas led to more equity selling?

Two good reasons. First, earnings came in just fine for Q1 and business didn’t hit the wall in March. If Starbucks and Chipotle are both reporting positive comps things just can’t be that bad. In March, during the sell-off, stocks were trading off what “should” happen. The reality of how consumers actually behaved proved better than expected. Markets had overshot, which is what they generally do.

Markets Are Behaving as they Should

Companies "smashed in the sell-off" came screaming back once fears proved overstated. This is the natural order of healthy markets: Buy improving companies. Avoid bad ones. Make money

Figuring out which companies are which, and investing accordingly, is literally how I fund my life. Sometimes I’m right, occasionally I’m wrong but as long as the world is conforming to the Natural Order I have no right to complain.

What Now? Be Long and Be Patient

Moments like this are when "rookies" make costly mistakes. They sell winners based on short-term charts to chase "fliers and garbage.

Last week, Amazon reported one of the great quarters in company history and shares actually fell. Newbies took a look at AMZN over the last month (“Up 30%!”) and bailed. They looked at Target, having its best year since the COVID bubble, and shifted money over the Lulu, figuring that’s where the “value” had moved.

Wrong. We’re in the 5th month of the year. We’ve had a macro Crisis Moment and a baby correction to go with it. We’ve got earnings from the retailers coming up in two weeks and by all indications the numbers will be ok… at least for the companies which have already started to turn their operations around.

The economy is strong enough to push improving companies higher but, by this point in the year if a 2026 turnaround was on the agenda it would already be showing signs.

There will be exceptions, and trying moments and maybe even a couple baby corrections. When the dust on 2026 the list of winners is going to consist largely of the companies that saw good price action and money inflows during the April comeback.

If you haven’t signed up already the time to do so is now, before we’re chasing these names higher.